The Ultimate Guide To Paul B Insurance

Table of Contents6 Simple Techniques For Paul B InsuranceSome Known Questions About Paul B Insurance.Not known Incorrect Statements About Paul B Insurance The Basic Principles Of Paul B Insurance Unknown Facts About Paul B InsurancePaul B Insurance Fundamentals Explained

represents the terms under which the claim will be paid. With residence insurance, for example, you might have a substitute expense or actual cash worth policy. The basis of just how claims are worked out makes a huge influence on just how much you earn money. You must constantly ask just how cases are paid and also what the insurance claims procedure will be.

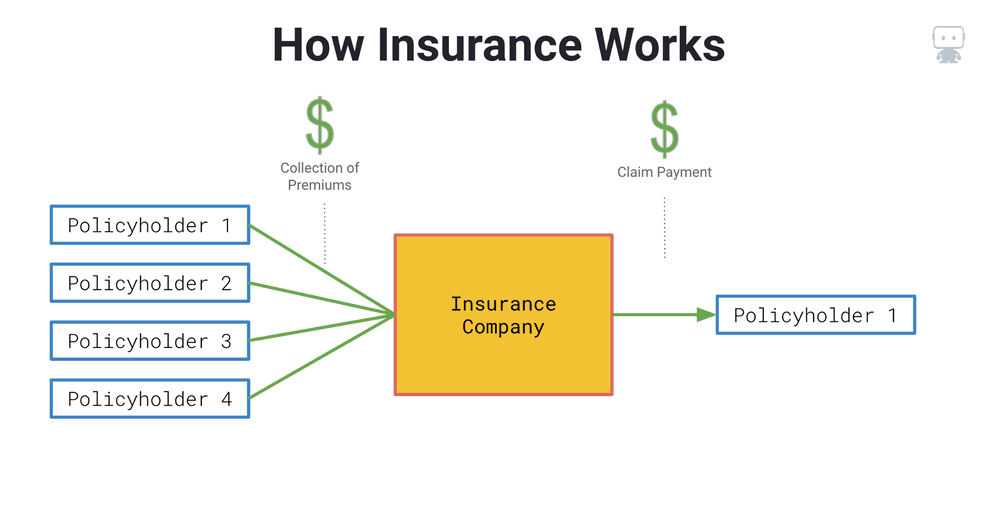

The thought is that the cash paid out in claims gradually will be much less than the overall premiums accumulated. You may really feel like you're throwing money out the home window if you never submit a case, however having piece of mind that you're covered in case you do suffer a significant loss, can be worth its weight in gold.

The smart Trick of Paul B Insurance That Nobody is Discussing

Picture you pay $500 a year to guarantee your $200,000 residence. You have one decade of paying, and also you've made no cases. That appears to $500 times ten years. This implies you've paid $5,000 for house insurance coverage. You begin to ask yourself why you are paying a lot for absolutely nothing.

Since insurance is based upon spreading out the risk amongst many individuals, it is the pooled cash of all individuals paying for it that allows the firm to construct possessions as well as cover cases when they happen. Insurance policy is an organization. Although it would certainly be good for the companies to simply leave rates at the exact same degree constantly, the fact is that they need to make enough cash to cover all the potential cases their insurance holders might make.

Underwriting modifications as well as price increases or decreases are based on outcomes the insurance firm had in past years. They offer insurance policy from only one firm.

The Greatest Guide To Paul B Insurance

The frontline people you deal with when you acquire your insurance are the representatives and also brokers that stand for the insurance policy firm. They an acquainted with that business's items or offerings, but can not talk in the direction of other companies' plans, pricing, or product offerings.

Exactly how much risk or loss of money can you think on your own? Do you have the money to cover your costs or debts if you have a crash? Do you have special demands in your life that need added coverage?

The insurance policy you need varies based upon where you go to in your life, what sort of assets you have, and also what your lengthy term goals as well as tasks are. That's why it is vital to put in the time to review what you want out of your policy with your representative.

Fascination About Paul B Insurance

If you get a lending to get a vehicle, and also after that something occurs to the cars and truck, gap insurance policy will certainly pay off any kind of section of your financing that standard automobile insurance policy does not cover. Some lending institutions require their borrowers to carry gap insurance.

The main objective of life insurance coverage is to offer money for your beneficiaries when you die. Just how you pass away can identify whether the more insurance firm pays out the fatality advantage. Depending upon the kind of policy you have, life insurance policy can cover: Natural deaths. Passing away from a cardiac arrest, disease or aging are examples of all-natural fatalities.

Life insurance policy covers the life of the insured individual. The insurance holder, who can be a different person or entity from the guaranteed, pays premiums to an insurer. In return, the insurance firm pays out a sum of money to the beneficiaries detailed on the policy. Term life insurance policy covers you for a time period chosen at acquisition, such as 10, 20 or 30 years.

Top Guidelines Of Paul B Insurance

Term life is prominent since it provides huge payments at a reduced price than permanent life. There are some variations of regular term life insurance policy plans.

Irreversible life insurance plans build money value as they age. The money worth of whole life insurance policies grows at a fixed rate, while the money value within universal policies can rise and fall.

$500,000 of whole life coverage for a healthy and balanced 30-year-old female costs around $4,015 yearly, on average. That exact same level of protection with a 20-year visit this page term life policy would certainly cost a standard of about $188 yearly, according to Quotacy, a brokerage firm.

Paul B Insurance Things To Know Before You Buy